Bring your own electrons

The hyperscalers have stopped waiting for the grid. The cost of replacing it is being quietly transferred to ratepayers.

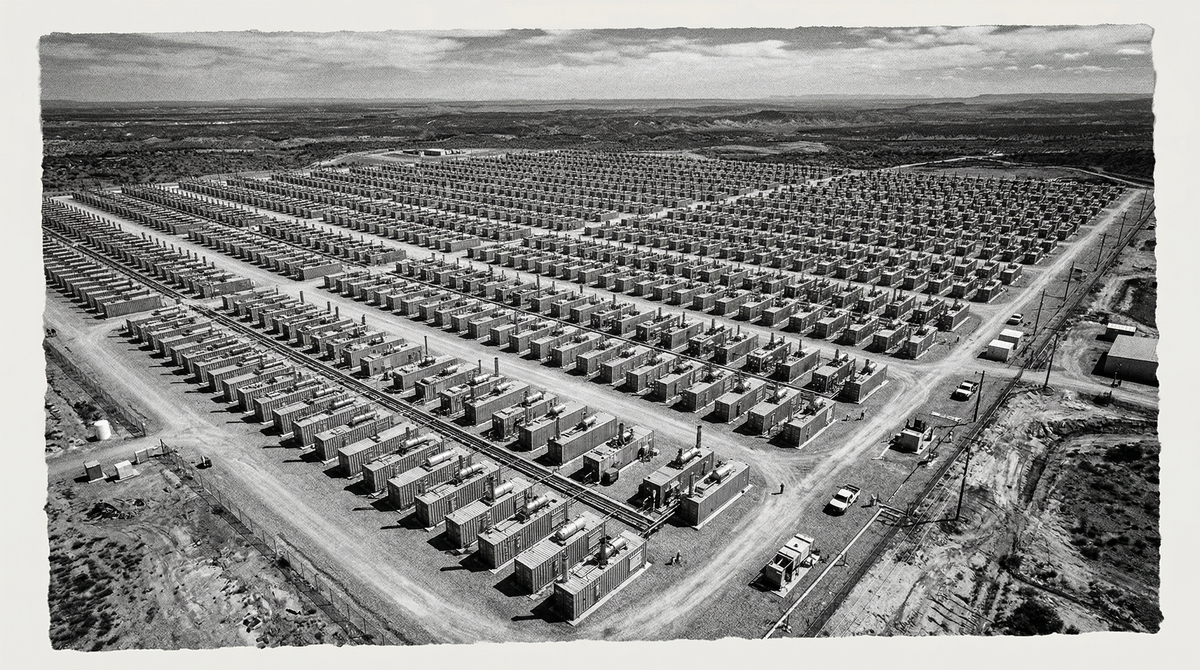

IN EL PASO, TEXAS, the local utility is preparing to install 813 small modular natural-gas generators in a single field to power Meta's $10bn data center next door. The Houston-based vendor that makes them — Enchanted Rock — usually sells the units to supermarket chains as backup for blackouts. Here they will be the primary generation, providing 366 megawatts to a single building. The cost of the plant is currently scheduled to be borne by Meta for one to five years; after that, it shifts to every other ratepayer in the El Paso Electric service territory.

The El Paso project is the visible end of an invisible reordering. By the end of 2025, American developers had announced approximately 40 behind-the-meter (BTM) data-center projects representing 48 gigawatts of capacity, according to Cleanview, an energy data firm. On-site data-center demand for new methane-gas generation rose from 5% of all such capacity at the end of 2024 to 39% a year later, with one year of on-site data-center demand for gas capacity outstripping all such demand from the prior year combined, per Stand.earth. Oracle's announcement on Monday that it would expand its Bloom Energy fuel-cell partnership to 2.8 gigawatts — Bloom's largest customer order ever — is the latest entry in a list that already includes Microsoft's gas plant in West Texas with Chevron and Engine No. 1 (potentially 5 GW), Google's 933 MW Crusoe gas plant in North Texas, and Meta's 7.46 GW Hyperion campus in Louisiana, alongside a $1.6bn Williams pipeline deal in Ohio and xAI's earlier expedient of trucking semitrailer-mounted generators to Memphis.

Plug and pray

The conventional read of all of this is that big tech is making a temporary detour around an overburdened utility system while it waits for the grid to expand. That framing is increasingly hard to defend. Bloom Energy delivered a megawatt-scale fuel-cell system to Oracle last year in 55 days, against a 90-day target; conventional natural-gas turbines deploy in two to three years from contract; the first small modular reactor sized for a data center is not expected before 2030, with most credible projects landing in the mid-2030s. PJM, the largest American grid operator, now averages eight years from interconnection request to commercial operation, even as its newly reformed Cycle process opens this month with a one-to-two-year study window — to which siting, permitting and construction must still be added. In an environment where unfulfilled cloud orders run into the tens of billions and frontier model training is bottlenecked on energized square footage, the cost of waiting has overwhelmed the cost of generating.

This article is for Vector members. Start a 7-day free trial to keep reading.

Start your free trial